Update 16:50 uur: Koop- en verkooplijstjes Goldman Sachs

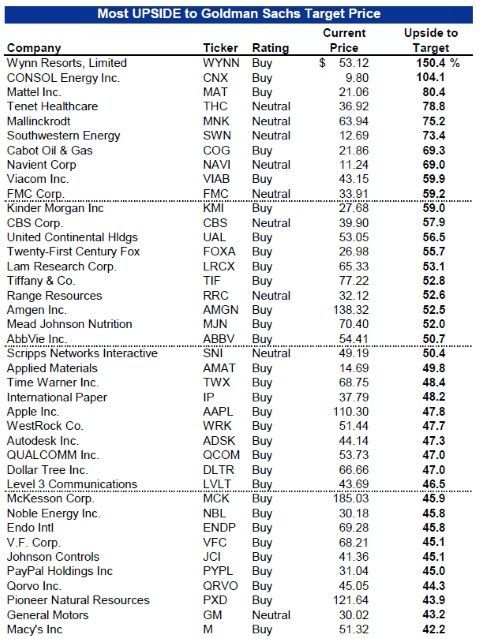

Via Bloomberg hebben we de koop- en verkooplijstjes van de S&P 500 aandelen van Goldman Sachs bemachtigd. Beginnen we met de aandelen met de meeste upside volgens The Firm.

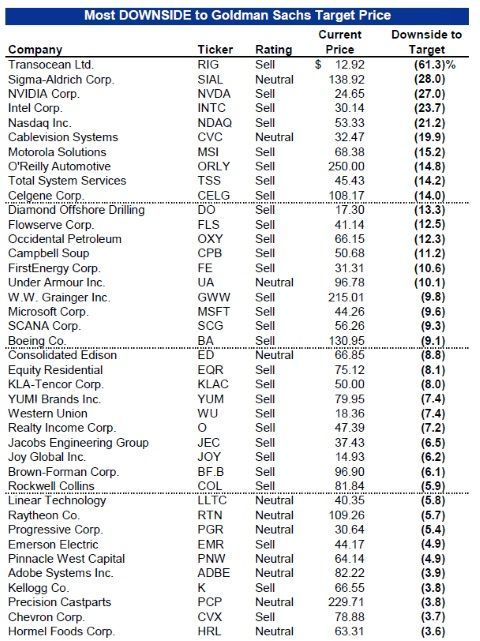

En de aandelen met de meeste downside volgens Goldman Sachs.

Update 15:50 uur: Renteverhoging

Maart dan maar?

(Nick)

Update 15:00 uur: S&P groei

Wat een schitterende lijst. Geen woord aan toe te voegen.

(Nick)

Update 13:50 uur: Air France-KLM

Nieuws over de mogelijke ontslagen van Air France-KLM:

(Nick)

Update 13:40 uur: Winstverwachting KW3

Winstverwachtingen voor het derde kwartaalcijferseizoen:

(Nick)

Update 12:30 uur: Adviezen

Goedemiddag, hier zijn de analistenadviezen van vandaaag. We hebben nog twee nieuwe toegevoegd.

- PostNL: koersdoelverlaging naar 4,80 van 5,50 euro (buy) - Jefferies

- Unilever: koersdoelverlaging naar 33,50 van 38,40 euro - JP Morgan

- Unilever: koersdoelverlaging naar 44 euro (kopen) - Bank of America Merril Lynch

- Delta Lloyd: koersdoelverlaging naar 7 van 16 euro (reduceren) - KBC

- Air France-KLM: downgrade naar reduceren van accumuleren en koersdoelverlaging naar 5,5 van 8,4 euro - Société Générale

(Nick)

Update 11:10 uur: Producentenprijzen

De producentenprijzen in de eurozone zijn verder gedaald

(Nick)

Update 09:15 uur: KBC over Fagron en Delta Lloyd

Nog altijd geen openingskoers, spannend! KBC Securities verhoogt het koersdoel van Fagron naar 26 van 20 euro (buy) en wel hierom:

While at this stage we have no insights on which parties could have approached Fagron, though we believe private equity players with an interest in healthcare could be most likely. In this respect, it is of interest to note that in 2012, Arseus was rumoured to have received a bid of € 15/sh at a time the company was trading at € 10.5/sh, and suggesting a valuation of around 9x EV/EBITDA.

We described in our note of 14 August that if Fagron would reach it FY15 ambitions (and mid single digit growth), it could be worth € 32/sh. The REBITDA outlook is now lowered by 15-20%, suggesting in model (and leaving everything else unchanged) a valuation range of around € 25-27/sh. Clearly, it is up to the potential acquirers and the current shareholders if this could be a matching price…

We expect a strong share price reaction today due to a combination of potential short coverage (estimated at >8.4%) and investors looking for a take-out premium. We take the acquisition interest serious and upgrade our target price to € 26/sh and BUY rating (from hold rating).

De Belgen wijden ook nog een zinnetje aan Delta Lloyd en zetten het koersdoel op 7 van 16 euro (reduce):

Based on our revised valuation approach, which now also incorporates a € 700m capital gap, we estimate the fair value at € 6.9ps.

(Arend Jan)

Update 08:10 uur: Ordina

Jan Niessen is voorgedragen als commissaris bij Ordina.

(Nick)

Update 08:00 uur: Fagron

Persbericht van Fagron is uit, er zou mogelijk interesse zijn in het fonds en Nico Inberg twitter er over:

(Nick)